When selling your home, you want to get the most money possible. In San Diego, we have fewer homes for sale than usual, so buyers are eager to find the right home that fits their budget and needs. They’re constantly checking real estate apps and talking to their Realtors to see what’s new on the market.

The first week your home is listed is when it gets the most attention. Buyers will look closely at all the photos and videos to see what type of upgrades the home has and check out its style, location, and curb appeal. That’s why professional photos are a must—you only have one chance to make a first impression. But even before they see the photos, the price is what truly catches their eye.

Pricing Your Home Right From the Beginning

Getting accurate pricing right from the start when selling your home is especially important now that the market is cooling down. Buyers today know what’s out there. They look at homes in all conditions, from perfect turn-key homes to fixer-uppers. They know a good deal when they see one. And they also know when a home is priced way out of line. If your home is priced too high, they’ll simply move on.

Once your home hits the market, buyers will quickly judge the asking price based on its condition. If it’s priced too high, many will skip seeing it in person. The longer your home stays unsold, the less excited buyers become. Even if you lower the price later, it won’t attract as much interest as a home priced right from the start.

While you might think that the price of your home will be primarily dictated by how much someone is willing to pay — often known as fair market value — establishing an asking price is key. It’s the starting point that influences how people view the property. If you overvalue it, people may be afraid or unwilling to place a bid, or worse, they might just scroll right past the listing without considering it at all.

Likewise, you don’t want to underestimate the value of your home, either. No seller wants to leave money on the table by choosing a lower price point than they had to. And if you go too low, buyers might assume there’s actually something wrong with the place.

Price Reduction Table

San Diego Market Trends and Stats

83% of homes in San Diego sold without reducing their asking price in May, with these homes selling for slightly above the asking price.

9% of homes had to reduce their price by 1-4% and took longer to sell, often selling for less than their original asking price.

8% of homes lowered their price by 5% or more and took nearly two months to sell, often for much less than the original price.

Expected Market Time – Days of Inventory Graph

The Impact of Market Time

The longer a home stays on the market, the less it typically sells for. Here’s what the data shows for homes in San Diego:

Homes sold in 10 days or less typically sold for $26,000 above the asking price.

Homes on the market for 11 to 30 days sold for about $13,000 below the asking price.

Homes listed for 31 to 60 days sold for around $29,000 below the asking price.

Homes on the market for 61 days or more sold for $46,000 less than the asking price.

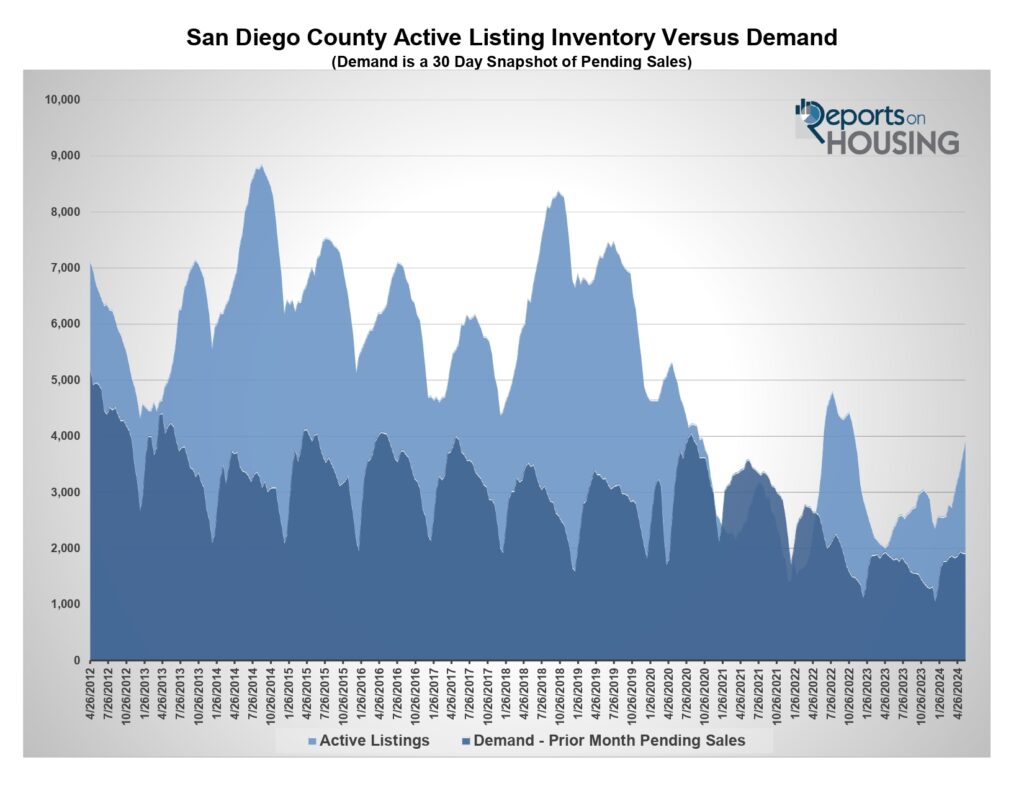

Active Listing Inventory vs Demand – Graph

Active Listings and Market Demand

The number of homes for sale in San Diego County right now has grown by 7%. While demand has stayed about the same, the time it takes to sell a home has increased. For example:

Homes priced under $750,000 are taking about 57 days to sell.

Homes priced between $750,000 and $1 million are selling in about 46 days.

Higher-priced homes, especially luxury ones, have varying times on the market, with some taking much longer to sell.

San Diego County Closed Sales Year Over Year – Graph

Closing Sales and Market Time in San Diego

In April, there were 2,095 closed sales, which is a 6% increase from the same time last year. Most of these were traditional sales with sellers who had equity.

Let’s Chat!

Thanks for tuning in! If you have any questions about the San Diego real estate market and accurate pricing when selling your home, don’t hesitate to reach out to a trusted local realtor like the McT Real Estate Group. We’re always here to help. Talk to you soon!

Recent headlines might have stirred questions about the trajectory of mortgage rates and what’s going on. Perhaps you’ve also heard murmurs of potential cuts this year, promising a downward shift in rates. This speculation typically revolves around the actions of the Federal Reserve (the Fed) and its management of the Fed Funds Rate. While adjustments to the Fed Funds Rate don’t directly dictate mortgage rates, they often exert influence. However, during the Fed’s recent meeting, no cut materialized — at least, not yet.

The Fed’s decision-making process involves numerous intricate factors, but you needn’t be overwhelmed by the complexity. What truly matters is the bottom line: does this signify a halt in the potential decline of mortgage rates? Here’s what you should keep in mind.

Mortgage Rates in San Diego Update – A Picture of A Group Talking at the Office

Anticipating Mortgage Rates Relief: Insights for San Diego Homebuyers

Mortgage rates are anticipated to decrease further this year, although the drop has yet to materialize. However, this delay doesn’t rule out the possibility of future reductions. Even Jerome Powell, the Chairman of the Fed, has affirmed the intention to implement cuts this year, contingent upon the moderation of inflation. This signals potential relief for prospective homebuyers in San Diego and beyond.

“We believe that our policy rate is likely at its peak for this tightening cycle and that, if the economy evolves broadly as expected, it will likely be appropriate to begin dialing back policy restraint at some point this year.”

When such occurrences unfold, historical trends indicate that mortgage rates will likely adjust accordingly. This implies that there is still optimism to be had. A recent article from Business Insider elaborates on this phenomenon.

“As inflation comes down and the Fed is able to start lowering rates, mortgage rates should go down, too. . .”

Mortgage Rates in San Diego Update – Two People Talking

What Does This Mean for You?

However, waiting for this shift may not be the best strategy. Predicting mortgage rates is notoriously difficult due to the multitude of influencing factors. Any fluctuation in the economy can swiftly alter projections. That’s why experts advise taking proactive steps. Mark Fleming, Chief Economist at First American, emphasizes the importance of staying informed and acting decisively.

“Well, mortgage rate projections are just that, projections, not promises and don’t forget how hard it is to forecast them. . . So my advice is to never try to time the market . . . If one is financially prepared and buying a home aligns with your lifestyle goals, then it could be the right time to purchase. And there’s always the refinance option if mortgage rates are lower in the future.”

If you’re considering a move and wondering about market timing, the best advice is: don’t wait. If you’re prepared, eager, and capable of making a move, seizing the opportunity now could prove beneficial, particularly if you discover the perfect home. In San Diego, where housing dynamics are vibrant, taking action when you’re ready can lead to securing your dream property.

Wrapping All Things Up on Mortgage Rates in San Diego

For those in the market to buy a home in San Diego, it’s crucial to stay informed about mortgage rates and make well-informed decisions. By reaching out and connecting with a trusted local realtor like the McT Real Estate Group, you’ll have a dedicated partner who will ensure you’re always in the loop regarding the latest mortgage rate updates. Let us guide you through the process, providing expert insights tailored to your needs and helping you confidently navigate the dynamic San Diego real estate market.

If you’re eagerly awaiting a housing market crash to bring San Diego’s home prices back down, it’s time to reassess and look at some data. The current data that we have paints a clear picture: a downturn isn’t on the horizon anytime soon. In fact, real estate experts predict that home prices will continue their upward trajectory through the coming months and years. Comparing today’s market to the pre-2008 housing crash reveals stark differences. This distinction is crucial in understanding why a repeat scenario is unlikely.

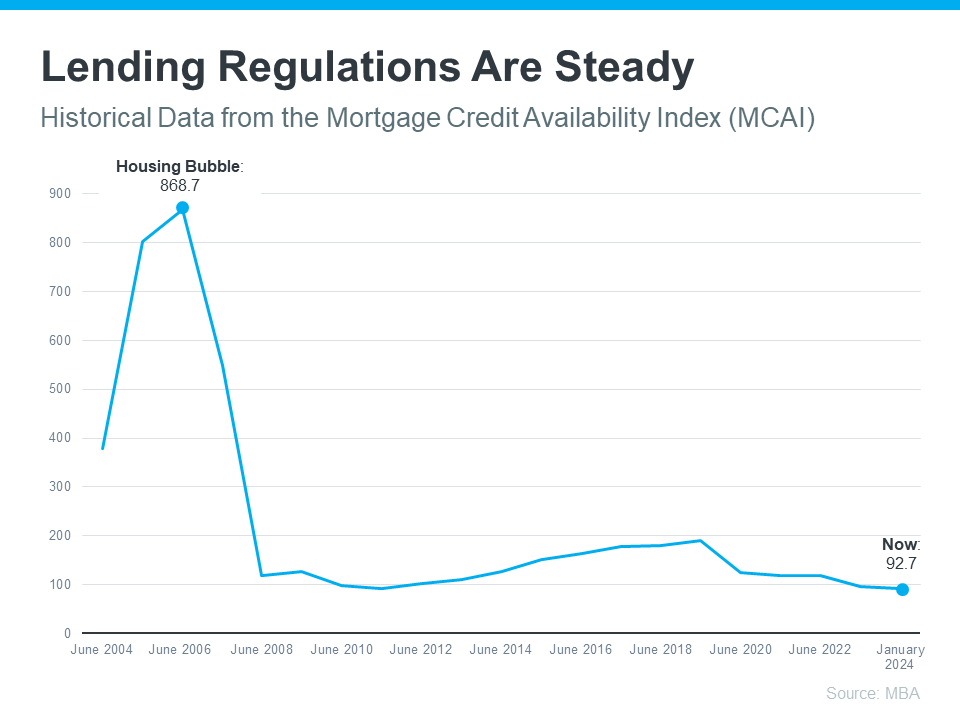

San Diego’s Evolving Mortgage Landscape: Navigating Stricter Standards for Homebuyers

Securing a home loan has become a more rigorous process in today’s real estate landscape, and surprisingly, this shift towards stricter lending criteria is a positive development. This is unlike the prelude to the 2008 housing crisis, where obtaining a mortgage was relatively effortless due to lenient standards set by banks. Banks have tightened their lending standards considerably, presenting a more selective environment for potential homebuyers. Unlike the past era, where almost anyone could qualify for a mortgage, today’s borrowers encounter heightened requirements from mortgage companies.

The Mortgage Bankers Association (MBA) data clearly shows this evolution in lending practices. A glance at the graph reveals a significant contrast in lending standards between then and now. The peak in the graph reflects a time when obtaining a mortgage was far less arduous, indicating lower barriers to entry into the housing market. However, the lax lending standards of the past era came with severe consequences. The surge in mortgage approvals without thorough vetting exposed borrowers and lending institutions to substantial risks. As a result, the market witnessed a wave of defaults and foreclosures, contributing to the infamous housing crash of 2008.

Lending Regulations Are Steady Graph

Today, San Diego’s real estate landscape is characterized by a more cautious approach, with lending institutions prioritizing responsible lending practices. This shift not only protects borrowers from entering unsustainable financial commitments but also safeguards the stability of the housing market. By imposing stricter standards, lenders mitigate the likelihood of another housing crisis, ensuring a more sustainable and resilient real estate environment for all stakeholders involved.

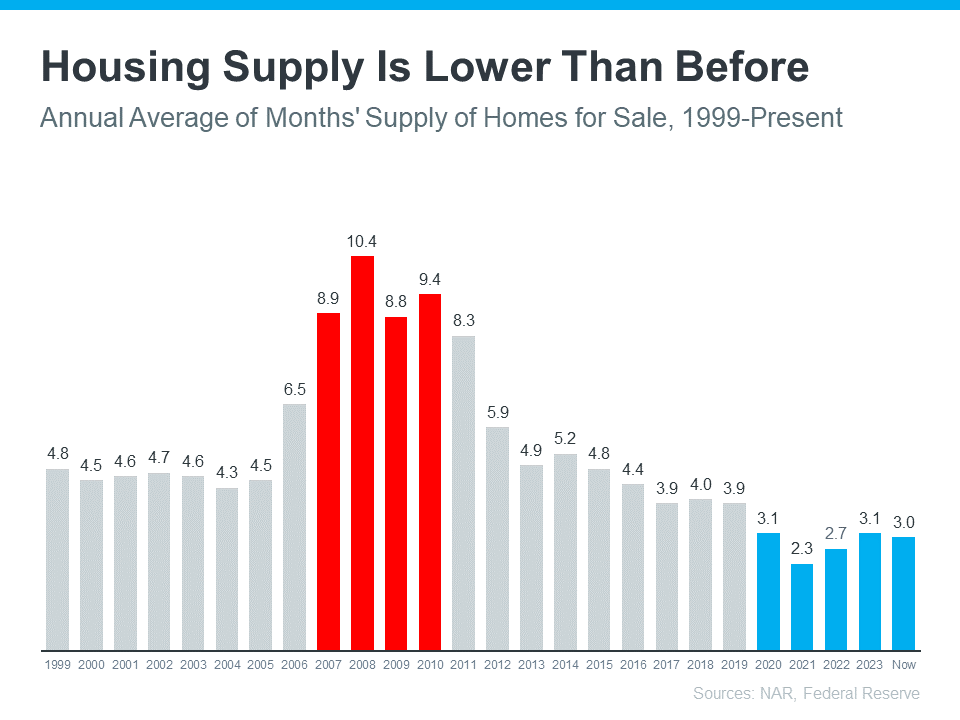

San Diego’s Housing Market Stability: A Closer Look at Inventory Trends

In today’s San Diego real estate market, we’re witnessing a significant shift from the conditions that led to the housing crash of the past. Back then, the market was flooded with an excess of available homes, many of which were distressed properties like short sales and foreclosures. This surplus in inventory drove home prices to plummet dramatically, causing widespread economic turmoil.

However, the landscape looks much different now. There’s a noticeable shortage of available homes for sale, creating a vastly different scenario from the conditions that precipitated the housing crisis. According to data sourced from reputable organizations such as the National Association of Realtors (NAR) and theFederal Reserve, the current inventory levels are strikingly low compared to the peak of the crisis.

For instance, the graph below illustrates the contrast between the months’ supply of homes available now (depicted in blue) versus during the housing crash (highlighted in red). Today, the unsold inventory hovers at a mere 3.0-months’ supply, a stark comparison to the peak of 10.4 months’ supply witnessed in 2008. This significant disparity indicates that there’s currently insufficient inventory on the market to precipitate a collapse in home prices akin to the events of the past.

Housing Supply is Lower Than Before Graph

In essence, the limited supply of homes for sale throughout the country safeguards against the risk of a housing crash, offering stability and confidence to buyers and sellers. As we navigate these evolving real estate dynamics, it’s evident that San Diego’s housing market is resilient and poised for continued growth and prosperity.

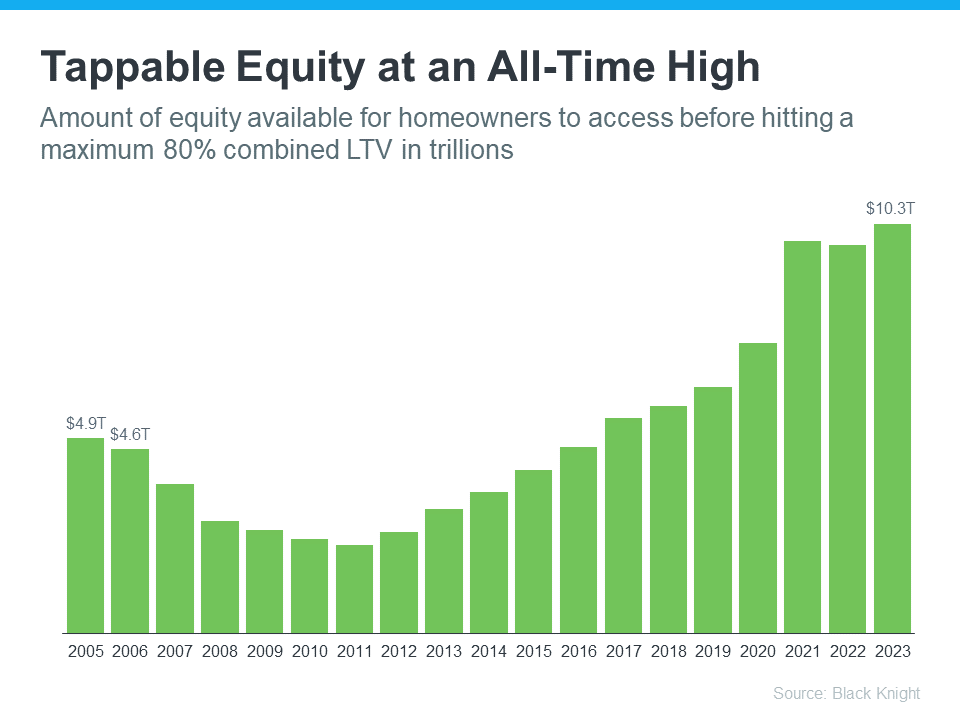

Fortifying Financial Resilience in Today’s Market

In the era leading up to the housing crash of the early 2000s, many homeowners utilized their homes as financial reservoirs, tapping into equity to fund various expenditures like new cars, boats, and extravagant vacations. Consequently, when property values plummeted, and housing inventory surged, numerous homeowners found themselves submerged in mortgages exceeding the value of their homes.

Fast forward to today’s real estate landscape in sunny San Diego, and a marked shift in homeowner behavior is evident. Despite the meteoric rise in property prices over recent years, homeowners exhibit a newfound prudence, refraining from extensive equity extraction akin to the pre-crash era.

According to data from Black Knight, tappable equity—representing the amount of equity accessible to homeowners before reaching an 80% loan-to-value ratio—has presently reached unprecedented levels. This surge in equity signifies that homeowners collectively possess more financial leverage than ever before, bolstering their financial resilience in the face of market fluctuations.

Tappable Equity at an All-Time High Graph

Moreover, Black Knight’s findingsunderscore this positive trend, revealing a significant decline in underwater mortgages.

“Only 1.1% of mortgage holders (582K) ended the year underwater, down from 1.5% (807K) at this time last year.”

With homeowners on firmer financial ground, the prospect of foreclosure diminishes, thereby curbing the influx of distressed properties into the market. Consequently, the absence of a deluge of inventory serves as a buffer against precipitous price declines, safeguarding the stability of San Diego’s real estate market.

Wrapping All Things Up

In summary, it’s normal to expect housing prices to drop, particularly in a lively city like San Diego. However, recent data shows otherwise. Unlike past downturns, San Diego’s real estate market is strong today. The newest studies clearly show that we’re not about to experience a housing crash like before. So, while people still want cheaper housing, the proof indicates that a crash isn’t coming soon.

In the ever-evolving landscape of San Diego mortgage rates, clarity amidst the confusion is crucial, especially for those eyeing the real estate market. Amidst the fluctuations, one trend stands out: a downward trajectory in mortgage rates compared to the near 8% peak experienced last fall. This trend bears significance for both prospective buyers and sellers alike, signaling a favorable environment.

While short-term volatility may sway rates based on economic indicators like inflation and reactions to the consumer price index (CPI), it’s essential not to lose sight of the bigger picture. Experts concur that the overarching trend points downwards, a reassuring sign for those navigating the housing market.

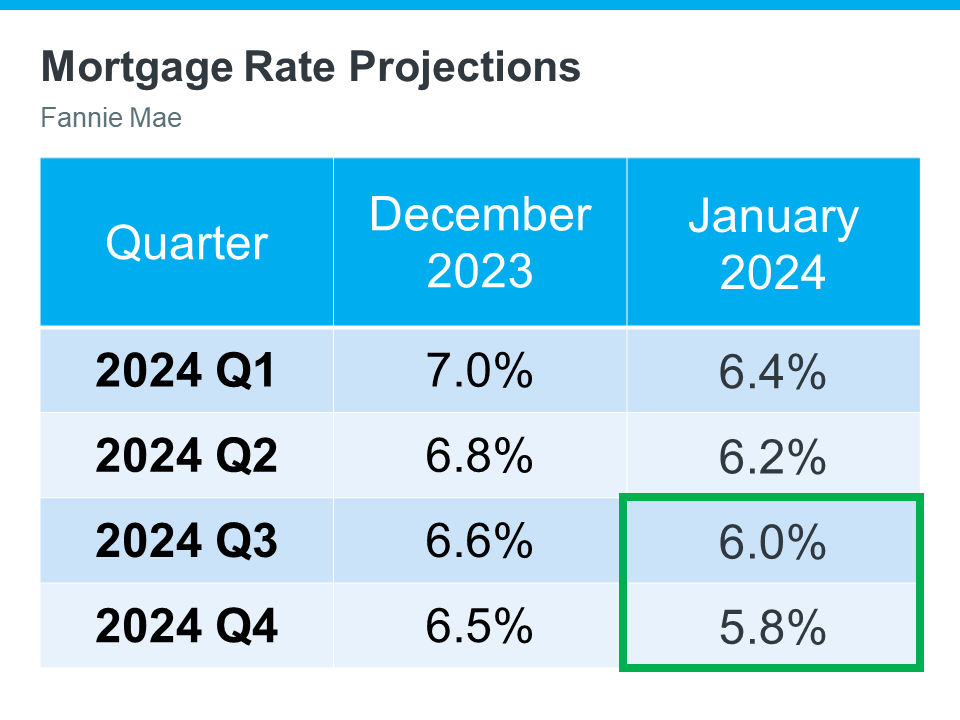

Looking ahead, projections hint at a potential milestone: mortgage rates dipping below the 6% mark later this year. Senior Economist Dean Baker of the Center for Economic Research lends credence to this outlook, suggesting a notable decrease from pre-Great Recession standards. Moreover, Fannie Mae’s latest projections align with this sentiment, offering optimism for prospective homebuyers (as illustrated in the chart below, highlighting projections in the green box).

“They will almost certainly not fall to pandemic lows, although we may soon see rates under 6.0 percent, which would be low by pre-Great Recession standards.”

Take a glance at the latest mortgage rate predictions for 2024, straight from Fannie Mae. This chart compares their December projection with the updated forecast just a month later. What catches the eye? A clear downward trend in the projections.

Mortgage Rate Projections Chart

It’s standard practice for experts to revise their forecasts as they closely monitor market dynamics and broader economic indicators. What’s evident here is a growing confidence among experts that mortgage rates will keep sliding, particularly if inflation eases.

In San Diego, where real estate trends often mirror national patterns, this shift could have significant implications for homebuyers and sellers alike. Lower mortgage rates typically mean increased affordability and heightened market activity, potentially sparking a surge in housing demand across the region.

What Does This Mean for You?

Remember that predicting the future of mortgage rates is not an exact science. Short-term fluctuations are normal, so it’s essential not to let minor changes unsettle you. Instead, maintain focus on the broader perspective. In today’s competitive San Diego market, finding a home that fits both your budget and your preferences can be challenging. If you’ve discovered a property you adore, waiting for rates to dip below 6% might not be the best strategy.

Considering current rates are already lower than last fall, you’re presented with a prime opportunity. Even a modest quarter-point decrease in rates can significantly enhance your purchasing power. So, seize the moment and make informed decisions based on market conditions.

To Wrap Things Up on the San Diego Mortgage Rate Forecast

In conclusion, if you’ve been delaying your move, anticipating a drop in mortgage rates, the current scenario suggests that the wait might be over. With rates potentially dipping below 6%, seizing the opportunity now could be the smart move. Ready to take the next step? Connecting with a trusted local real estate team like the McT Real Estate Group in San Diego can help you kickstart the process. And hey, if you’re considering a move in the vibrant San Diego area, there’s no better time to explore your options!

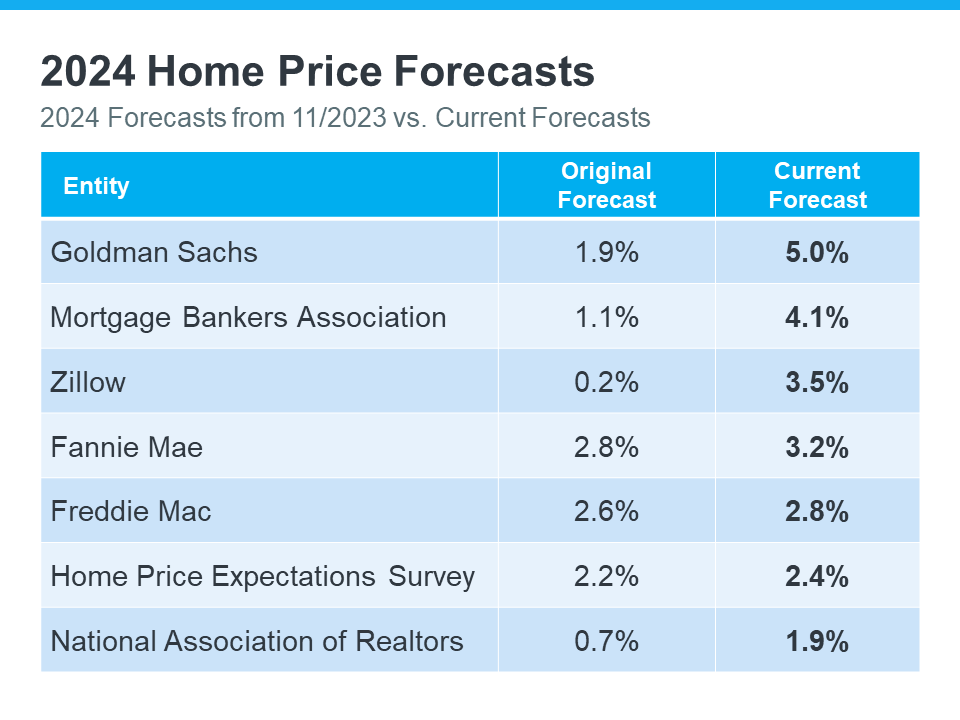

In recent months, experts have reviewed their 2024 home price forecasts, drawing from updated data and market indicators. Their confidence in price escalation has only strengthened. Now, let’s dive into the nuanced adjustments in experts’ perspectives and explore the driving factors behind this shift, particularly within the vibrant real estate landscape of San Diego.

2024 Home Price Forecasts: Then vs. Now

Analyzing San Diego’s housing market and comparing initial 2023 projections with recent revisions from top experts is insightful. Initially, modest price increases were expected, but now, all forecasters anticipate more significant hikes. This shift reflects ongoing trends: a persistent shortage of homes for sale and recent decreases in mortgage rates. These factors reignite buyer interest and prompt experts to anticipate stronger price growth.

Check the chart below for insights into San Diego’s 2024 home price trends. We’ve compiled predictions from seven leading expert organizations, showcasing their initial forecasts from the end of 2023 and their latest projections. This data offers a comprehensive view of the evolving landscape, empowering you to stay ahead in the real estate market.

2024 Home Price Forecasts Chart

In the initial assessments, experts anticipated only marginal increases in home prices for the current year, as indicated in the middle column. However, upon closer examination of the updated forecasts in the right column, it’s evident that these projections have undergone significant revisions, now pointing towards more substantial price escalations than previously anticipated.

The surge in home prices is attributed to two prominent factors exerting considerable upward pressure. Firstly, the persistentlylow inventory of homesavailable for sale remains a chronic challenge nationwide. As highlighted by Business Insider, this scarcity in housing supply has consistently upheld home prices, driving them upwards.

“Low home inventory is a chronic problem in the US. This has generally kept home prices up . . .”

Fast forward to the present, and we observe a significant change in the landscape. Mortgage rates have softened since their peak in October, and further decreases are anticipated throughout the year. Consequently, buyer demand has surged. This uptick in demand and the persistent scarcity of housing inventory have prompted experts to revise their forecasts. They now anticipate a stronger upward pressure on prices than just a few months ago.

Getting Ahead of the Home Price Next Forecast

Looking ahead to stay ahead of the curve in the ever-evolving real estate landscape is crucial. Real estate professionals update home price forecasts to keep pace with market dynamics. This process ensures their predictions remain accurate and reflect current housing market trends.

As the housing market evolves, these experts will persist in revising their projections. This practice is essential for adapting to fluctuations and integrating the latest market shifts into their forecasts. Anticipating these revisions is key to staying informed and making well-informed decisions.

In real estate, particularly in San Diego, where market conditions vary, keeping an eye on mortgage rates is paramount. As mortgage rates are anticipated to decrease throughout the year, it could stimulate heightened buyer demand and impact home price forecasts.

Essentially, the supply and demand principle governs the housing market dynamics. Given the persistently limited supply, any factors boosting demand will likely drive prices upward. This interplay underscores the importance of closely monitoring market indicators and adapting strategies accordingly. Homeowners and buyers can navigate the market effectively and capitalize on emerging opportunities by staying attuned to these trends.

To Wrap Things Up

In conclusion, initial predictions suggested only marginal growth in home prices for the year. However, recent expert updates reveal a significant expectation shift, with projections indicating even stronger price escalations than anticipated. This adjustment underscores the dynamic nature of the real estate market, particularly in vibrant locales like San Diego. As these forecasts evolve, it becomes increasingly crucial for homeowners and prospective buyers to stay informed about the shifting landscape. Reach out to the McT Real Estate Group today to gain valuable insights into how these developments may impact pricing trends within our local market.

Decoding the Mortgage Rollercoaster: Navigating Rates in San Diego’s Vibrant Market

San Diego’s real estate scene is as colorful and dynamic as a sunset over the Pacific, and mortgage rates can seem to mirror that very same energy. One minute you hear whispers of them dropping, the next they’re supposedly skyrocketing out of nowhere – enough to leave even the most seasoned homeowner with a dizzy head with all these ups and downs. But fear not, fellow San Diegans! We’re here to clear the confusion and help you navigate this ever-shifting landscape.

The truth is, that the mixed messages often stem from the specific timeframe being analyzed. What appears like a dramatic upswing over a week might be a gentle decline compared to last year’s peak. That’s why, instead of getting lost in the day-to-day fluctuations, we need to take a step back and zoom out. Let’s delve into the unique dynamics of San Diego’s mortgage market and shed some light on the bigger picture. Shall we?

Mortgage Rates: A Journey Through Peaks and Valleys

Think of mortgage rates as a San Diego roller coaster – exciting, unpredictable, and influenced by a whirlwind of factors. From the Federal Reserve’s decisions to global economic shifts, these rates are in constant motion. What goes up today might come down tomorrow, making any short-term analysis a bit of a guessing game.

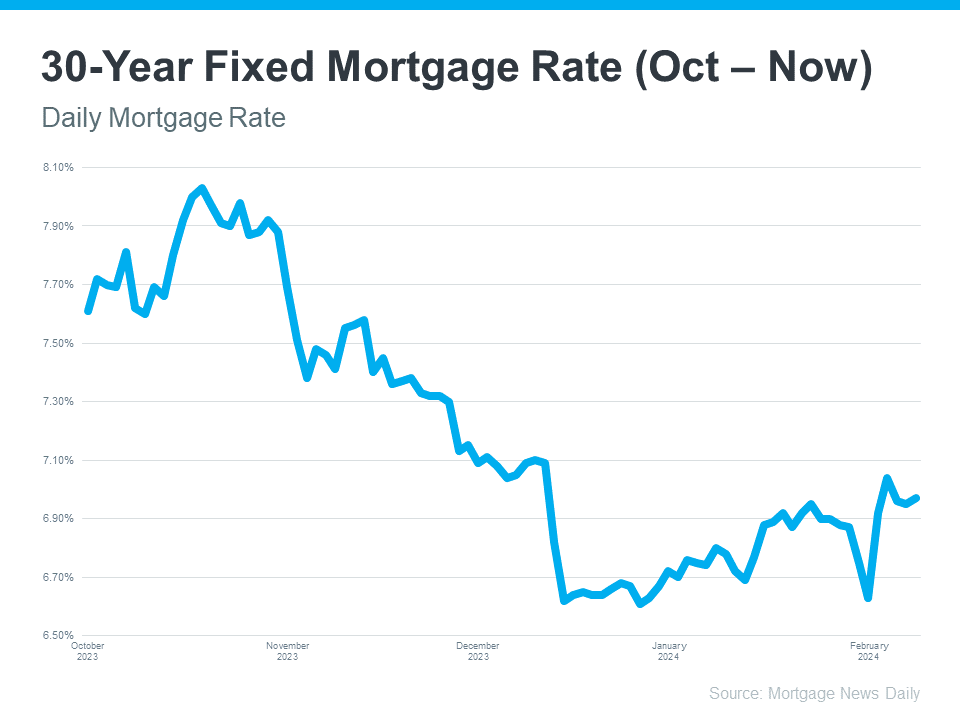

To illustrate this point, let’s peer into a graph charting the 30-year fixed rate since last October. It’s a wild ride, mirroring the ups and downs of our beloved city’s economy. But don’t get discouraged by the dips! Zooming out, we see that compared to October’s peak, rates have actually been on a gradual decline. Now, the question becomes: how do we interpret these fluctuations in the context of San Diego’s vibrant real estate scene?

30-Year Fixed Mortgage Rate Line Graph

Focusing solely on the past week might make it seem like rates are inching upward. However, when we compare them to the October high, the overall trend reveals a welcome decrease. This perspective shift is crucial, especially in a dynamic market like San Diego. Whether you’re a seasoned homeowner or a first-time home buyer, understanding these trends empowers you to make informed decisions.

The Good News: A Glimpse into the Future

Stepping away from the daily rollercoaster, we see a more promising picture. Industry experts project this downward trend to continue throughout the year, offering a beacon of hope for prospective San Diego buyers. While temporary fluctuations are inevitable, focusing on the bigger picture ensures you’re not swayed by momentary blips.

Ready to Navigate the Ride? We’re Here to Help!

The world of mortgage rates can be a wild ride, but you don’t have to go it alone. Whether you have questions about the latest San Diego homes or just want to clarify the mortgage jargon, a seasoned local real estate team like the McT Real Estate Group is here to be your expert guide. So, buckle up, San Diego – let’s navigate this exciting market together!

Are you feeling anxious about the current buzz surrounding San Diego’s Market Trends on Home Prices? It’s crucial to remember that these headlines only provide a glimpse of the overall narrative.

Contrary to what you might have heard, the national data paints a different picture. In fact, home prices exhibited positive growth throughout the year. While there were minor fluctuations in certain markets and occasional dips in some months on a national scale, these instances were more of an anomaly than a trend.

The bottom line? Last year saw an upward trajectory in home prices, not a decline. It’s time to delve deeper into the data to gain a clearer understanding of the situation in San Diego and beyond. Let’s separate fact from fiction and explore the real story behind the numbers.

Understanding 2024 Return to Normal Home Prices

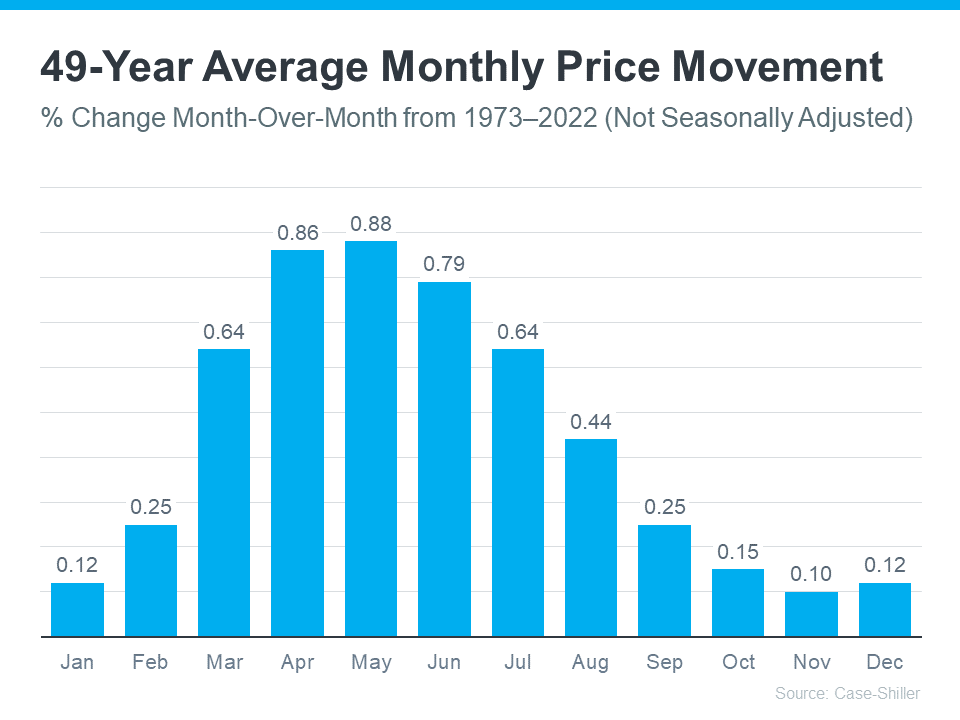

In 2023, we witnessed a return to more typical home price growth, marking a step toward normalization in the housing market. Understanding this trend requires delving into the predictable ebbs and flows inherent in residential real estate, a phenomenon known as seasonality.

Traditionally, spring emerges as the peak homebuying season, characterized by heightened market activity. Summer maintains this momentum before a gradual decline sets in towards the year’s end. Correspondingly, home prices tend to surge during periods of high demand, aligning with the ebbs and flows of the market.

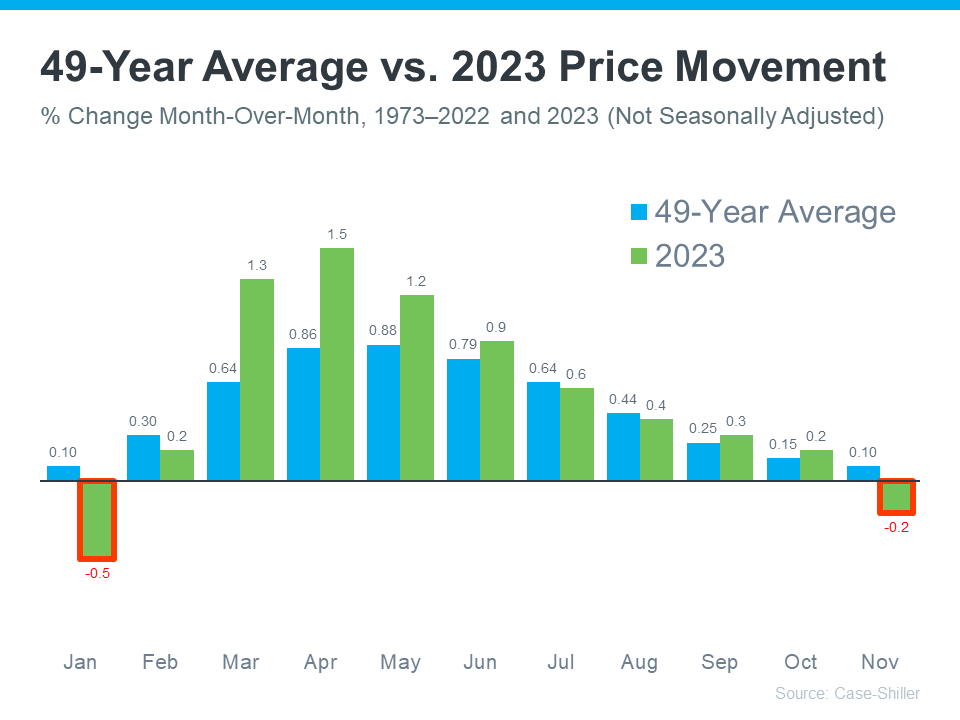

49-Year Average Monthly Price Improvement Graph

Analyzing data fromCase-Shillerspanning nearly five decades unveils a consistent pattern of home price fluctuations mirroring market seasonality. At the onset of each year, prices exhibit moderate growth, reflecting decreased market activity during the winter months. As spring ushers in the peak homebuying season, both market activity and home prices escalate. Conversely, as autumn approaches, market activity recedes, resulting in slower price growth.

49-Year Average vs 2023 Price Movement Graph

Examining the data for 2023, illustrated by the green bars atop the long-term trend (depicted in blue), reveals a convergence with historical trends on home prices as the year progresses. Notably, the green bars closely align with the blue bars in the latter part of the year, indicating a more consistent level of appreciation.

Despite this nuanced analysis, media headlines predominantly spotlighted specific data points, overlooking broader contextual insights. It’s crucial to understand that moderate price adjustments during fall and winter months are typical, reflecting seasonal patterns. Considering the 49-year average, which hovers close to zero during these periods, slight declines are not uncommon and should be viewed as transient fluctuations within a broader upward trajectory in home prices throughout the year.

What You Should Keep in Mind

Rather than getting caught up in the minor fluctuations from month to month highlighted in headlines, it’s crucial to look at the broader, year-long trends. Focusing solely on these short-term changes can paint an incomplete picture of the real estate market.

Consider the shift we witnessed last year, where seasonality returned to the housing market—a positive development following the unsustainable surge in home prices during the pandemic’s peak years.

And if you’re concerned about a potential decline in home prices, rest assured that such worries may be unfounded. Projections for this year suggest that prices will continue to rise. This expectation stems from factors such as decreasing mortgage rates compared to last year, enticing more buyers back into the market. Simultaneously, the supply of homes for sale remains limited, further driving up prices as demand intensifies.

In San Diego, these trends hold particularly true, with the local market exhibiting similar dynamics. Understanding these broader trends can provide a clearer perspective for homeowners and prospective buyers alike, allowing for more informed decisions in navigating the real estate landscape.

Bottom Line on San Diego’s Market Trends

Essentially, it’s crucial not to get bogged down by the barrage of home price updates flooding the media. Looking at the broader picture, 2023 witnessed a notable uptick in home prices. However, amidst the flurry of headlines, it’s easy to feel overwhelmed or uncertain about what these fluctuations mean for our local market here in San Diego.

Should you find yourself grappling with questions sparked by these news snippets or overthinking the intricacies of home price dynamics in our city, don’t hesitate to reach out to the McT Real Estate Group. Let’s engage in a conversation tailored to your concerns and delve into the specifics of San Diego’s real estate landscape. Your peace of mind matters, and we’re here to provide the insights and support you deserve. Let’s connect and unravel the mysteries surrounding home prices in San Diego.

In the changing world of estate, in Southern California people looking to buy a home are facing a tough challenge due to the sharp increase in financial pressures over the last couple of years. It’s not about housing; it’s also about dealing with higher costs, rising mortgage rates, and the big question of whether it’s affordable. Let’s dig deeper into this issue by examining data from the California Association of Realtors and how Federal Reserve policies play a role.

Affordability Challenges Across Southern California

Affordability Challenges Across Southern California

The financial barrier for homebuyers in Southern California has significantly risen. To put things into perspective, someone wanting to buy a home by 2023 would need an annual income of $207,000, which is a notable increase from the $134,000 required just two years ago. This 55 percent rise in income shows how much harder it has become to own a home.

This challenging situation is caused by factors. The median price for an existing single-family home reached $775,000 by the end of 2023, marking a 7 percent increase from two years earlier. While in North Park and other metro neighborhoods in San Diego, the median price is $1,207,000. What is more impactful is that average mortgage rates have more than doubled, going up from 3.3 percent up to 7.4 percent, dramatically changing the costs involved in purchasing a house.

As a result, the estimated monthly payment for a home has experienced a sharp increase of $1,830, elevating the monthly financial obligation to $5,180. If one is buying a home in the San Diego metro communities, such as North Park, South Park, University Heights, and others, just know that if you are putting 20% down on a median-priced home, your monthly mortgage payment will be approximately $9,000.00 dollars.

The Rising Financial Barriers

The Rising Financial Barriers

These changes have significantly impacted affordability, reaching its levels since before the Recession. Only 14 percent of households in Southern California are now able to afford a median-priced home by the end of 2023. This marks a decrease from the 26 percent affordability rate observed at the close of 2021, reflecting the challenges of the housing market bubble in the mid-2000s.

When looking at California as a challenge, the required income to purchase a home in the state of California stands at $223,000 for an $833,000 property, which is somewhat better than Southern California but still daunting. In contrast, despite housing costs and tech salaries in the Bay Area, a higher income is needed for purchasing a house compared to other regions; however, it offers slightly improved affordability rates compared to Southern California and the state overall.

Diving into areas within Southern California reveals differences from Orange County’s increase in necessary income amounting to $134,000, all the way to San Bernardino’s relatively modest hike of $47,000. This regional breakdown underscores how diverse the affordability crisis is across counties.

Despite facing these odds, there is hope due to the decrease in mortgage rates to approximately 6.7 percent. This could reduce the income threshold for individuals looking to purchase homes in Southern California. However, this small progress does not significantly change the situation, especially when compared to the perspective where the average American’s ability to afford homes is notably better.

Opportunities Needed to Buy a Home in Southern California

Opportunities Needed to Buy a Home in Southern California

The main issue is this: owning a home in Southern California is becoming an aspiration for many people, as demonstrated by historically low home sales. While slight shifts in mortgage rates provide some respite, the broader affordability crisis calls for solutions and continued focus to bridge the gap between the dream of homeownership and the reality faced by residents of Southern California.

Despite the real estate environment, in San Diego, there is an aspect for individuals aiming to navigate the market. Sellers can take advantage of the rising home values to benefit from their investments. Potentially earn a great deal of profits.

With recent decreases in mortgage rates, there is a ray of hope, making this a promising time to enter the market. Additionally, San Diego’s enduring charm, including its communities and breathtaking natural surroundings, continues to make it a sought-after place to reside.By implementing strategies seeking advice from real estate professionals and focusing on long-term value, buyers and sellers can work towards their real estate objectives by transforming challenges into opportunities within this dynamic market.

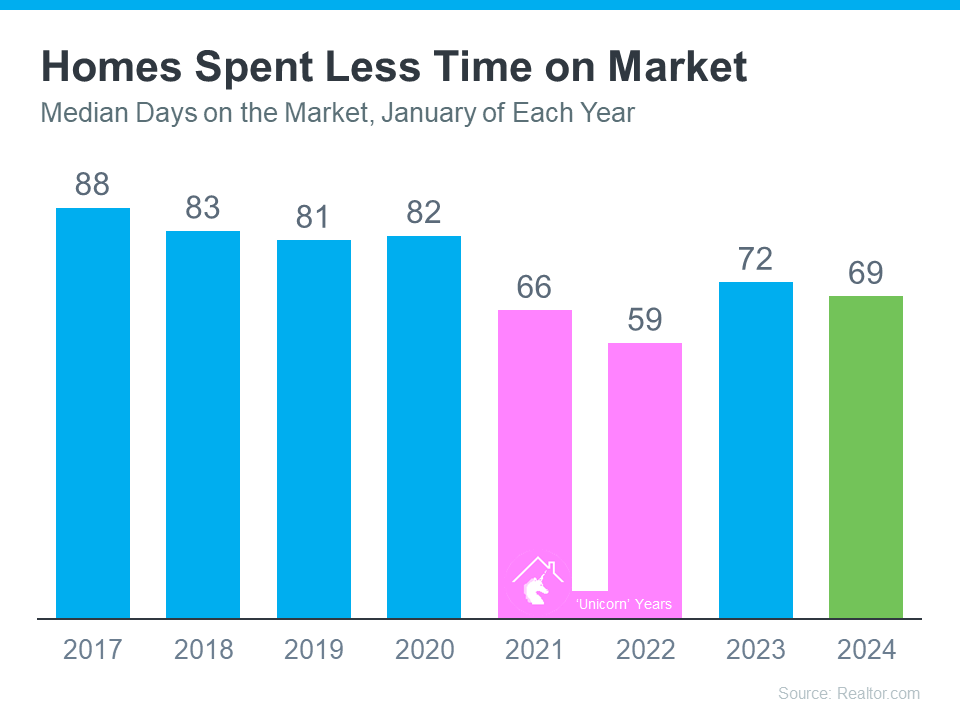

Thinking of selling your home in San Diego? Good news awaits you! The real estate scene, while no longer at its ‘unicorn’ peak where homes flew off the market in record time, is still buzzing with swift sales.

To paint a clearer picture, let’s dive into some insightful data from Realtor.com. We’ve charted the median days on the market for homes each January from 2017 to the most recent stats. “Days on the market,” in this context, tracks the time from a home’s listing to its closing or removal from the market. This key metric sheds light on the pace of sales in comparison to typical years.

Homes Spent Less Time on Market Graph

Now, focusing on the latest data (highlighted in green), we observe a trend: homes Nationwide are selling quicker than usual (represented in blue). The only period that outpaced the current market speed was during those extraordinary ‘unicorn’ years (indicated in pink). This is a significant drop from last year’s average of 27 days, pointing towards a very active market where listings move quickly. In San Diego, the numbers are a little different. San Diego, as a whole, homes have been hitting the pending status in about ten days, with the entire sale process wrapping up in roughly 18-21 -days. Here’s what Realtor.com’s findings tell us about the US market right now:

“Homes spent 69 days on the market, which is three days shorter than last year and more than two weeks shorter than before the COVID-19 pandemic.”

This trend offers a compelling opportunity for San Diego homeowners. Whether you’re in the heart of the city, in the metro neighborhoods such as North Parkand South Park, or nestled in its nearby suburban neighborhoods, the market’s momentum is in your favor. As your local real estate experts, we’re here to guide you through this dynamic market, ensuring you make the most of these fast-paced selling conditions.

Homes Selling Fast in San Diego

Right now, the real estate market in San Diego is buzzing with activity, meaning your home could be the next hot listing. With the recent dip in mortgage rates, there’s been a surge in potential buyers eager to make a move. However, the supply of homes hasn’t quite caught up with this growing demand. Mike Simonsen, the Founder of Altos Research, highlights this trend, noting:

“. . . 2024 is starting stronger than last year. And demand is increasing each week.”

San Diego Market Update

Final Thoughts

Take a look at our latest market update for both San Diego County and one of our favorite metro neighborhoods, North Park.

North Park Market Update

Are you considering selling your home and are curious about the right time to do so? The latest market trends indicate that now might be an excellent opportunity. Currently, the San Diego real estate market is showing remarkable strength, more so than what’s typically expected during this season. For up-to-date insights specific to our local market, feel free to reach out to the McT Real Estate Group. Let’s connect and explore your options together.

Have you come across sensational headlines discussing a surge in foreclosures within today’s real estate market? If these articles have left you with a sense of uncertainty about the future and what to do, it’s essential to recognize that such clickbait titles often lack the comprehensive context needed to make some well-informed decisions.

In reality, when you juxtapose the present data with historical market trends, you’ll quickly realize that there’s no cause for alarm. These headlines tend to focus on isolated events rather than the broader, more stable market picture. By considering the bigger picture, you can make more confident and well-informed decisions regarding your real estate endeavors. Rest assured, that San Diego foreclosure rates remain below average and continue to exhibit resilience and offer opportunities for both buyers and sellers alike.

Putting the Headlines into Perspective

The media’s recent emphasis on the increase in foreclosure rates can be somewhat misleading. This emphasis arises from their comparison of current figures to a period when foreclosures were at historically low levels, creating an impression of greater significance than the actual situation warrants.

In the years 2020 and 2021, a combination of the moratorium and forbearance programs proved instrumental in assisting countless homeowners in maintaining their residences. These initiatives provided a lifeline, allowing homeowners to regain their financial footing during an exceptionally challenging period or what we usually refer to as the pre and post-pandemic years.

With the conclusion of the moratorium, it was only natural to anticipate a rise in foreclosure numbers. However, it’s important to note that an increase in foreclosure rates doesn’t necessarily signal trouble in the housing market. It’s more a return to a more typical state of affairs rather than an impending crisis

Based on Data There Isn’t a Wave of Foreclosures Coming Anytime Soon

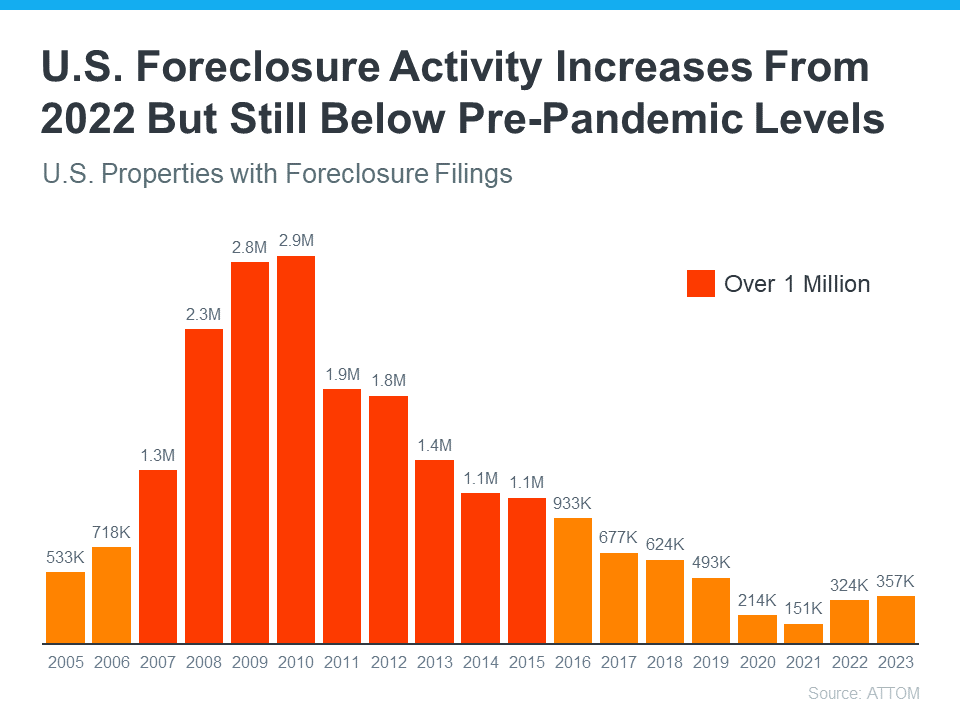

Let’s dig into the historical data to gain a clearer perspective on the current foreclosure situation. Instead of merely comparing recent figures to the anomalies of the past few years, a more insightful approach is to assess the long-term trends—specifically, those stemming from the housing market crash, a concern many share.

Direct your attention to the graph below, which draws on foreclosure data sourced from ATTOM, a trusted property data provider. The chart distinctly illustrates that foreclosure activity has consistently remained at lower levels (depicted in orange) since the tumultuous events of the 2008 housing crash (highlighted in red)

US Foreclosure Activity Increases From 2022 But Still Below Pre-Pandemic Levels Graph

Now, let’s dive into the recent report on foreclosure filings. Although there has been an increase in these filings, it’s crucial to emphasize that the current situation bears no resemblance to the past housing crisis. In fact, we haven’t even reached the foreclosure rates seen in more typical years, such as 2019. Rick Sharga, Founder and CEO of the CJ Patrick Company, sheds light on this:

“Foreclosure activity is still only at about 60% of pre-pandemic levels. . .”

This trend primarily results from today’s buyers having stronger qualifications, making them less prone to loan defaults. Delinquency rates continue to remain at minimal levels, and the majority of homeowners possess substantial equity, safeguarding them from foreclosure. As Molly Boesel, Principal Economist at CoreLogic, aptly states:

“U.S. mortgage delinquency rates remained healthy in October, with the overall delinquency rate unchanged from a year earlier and the serious delinquency rate remaining at a historic low… borrowers in later stages of delinquencies are finding alternatives to defaulting on their home loans.”

In reality, although foreclosure rates are on the rise, the current market situation doesn’t indicate a full-blown crisis. Instead, it signals a shift in the market’s trajectory. The data reveals that we’re not currently facing a foreclosure crisis, nor is it the direction in which the market is moving

Conclusion on San Diego Foreclosure Rates

In summary, while the housing market is currently witnessing a predicted increase in foreclosures, it’s essential to stress that we are far from the dire crisis levels that occurred during the housing bubble collapse. These fluctuations are part of a natural market ebb and flow. If you find yourself perplexed by the information you come across regarding the housing market, don’t hesitate to reach out to an expert local real estate team like the McT Real Estate Group; We’re here to provide you with clarity and guidance, ensuring you make informed decisions during this dynamic real estate landscape.