How should North Park homeowners handle economic uncertainty in 2026? By separating national headlines from local data, understanding what is actually happening in 92104, and making decisions based on your own life situation rather than fear or pressure.

Selling my home in North Park is a thought that has crossed many homeowners’ minds lately. So has the opposite thought: “I should probably just stay put until things calm down.”

Both thoughts are valid. And both deserve better information than what cable news and social media are giving you.

Tariff headlines. Recession rumors. Stock market swings. Insurance costs are climbing. It is a lot. And when you are sitting on what is probably your largest financial asset, all that noise makes every decision feel heavier than it should.

This post is not here to tell you to sell. It is not here to tell you to stay. It is here to give you real data about what is happening in North Park and San Diego right now so you can think clearly about your own situation, whatever that looks like.

You Are Not Alone in Feeling Uncertain

If the economy has you feeling uneasy about big financial decisions, you have a lot of company.

A Bright MLS survey of 3,300 adults found that over 80% of homeowners are worried about needing to cut essential spending in 2026. A separate HomeLight survey of 850+ real estate agents found that economic uncertainty was one of the top five concerns homeowners are raising this year.

And 41% of homeowners told the IPX1031 Homeownership Report that high interest rates have turned their current home into a “forever home,” whether that was the original plan or not.

That hesitation makes sense. When the ground feels unsteady, the natural response is to freeze and wait for clarity. There is nothing wrong with that instinct. The key is to make sure “waiting” is an active, informed choice, not just a reaction to fear.

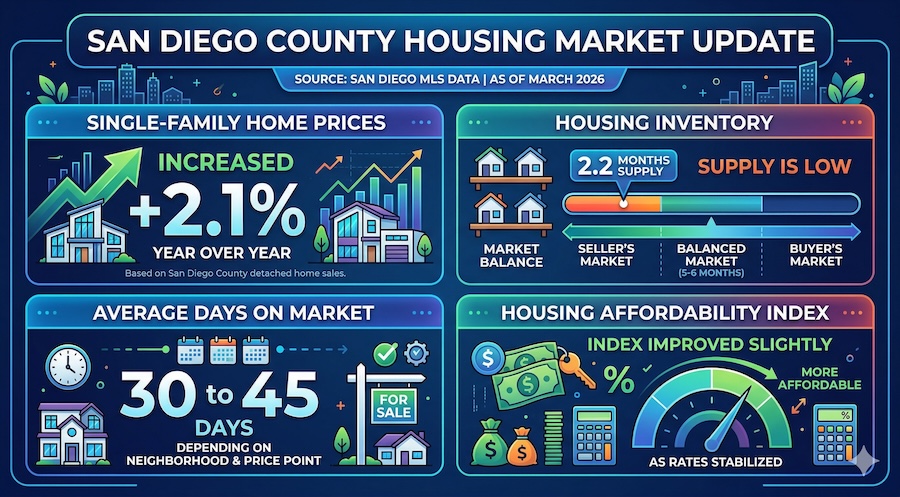

What Is Actually Happening in the San Diego Housing Market

National headlines paint a broad picture. Your home does not fit into a broader picture. It exists on a specific block in a specific zip code. So here is what the local data says.

According to San Diego MLS data as of March 2026:

- Single-family home prices in San Diego County increased 2.1% year over year

- Inventory sits at 2.2 months of supply. A balanced market typically has 5 to 6 months.

- Average days on market is 30 to 45 days, depending on neighborhood and price point

- The housing affordability index improved slightly as rates stabilized

North Park and its neighboring communities, including South Park, University Heights, Golden Hill, and Normal Heights, remain some of the tightest-supply areas in the county. Limited buildable land, historic housing stock, and strong lifestyle demand keep these neighborhoods relatively stable even when other parts of the market soften.

J.P. Morgan Global Research projects U.S. home prices will remain flat nationwide in 2026. But they also note that tight-supply urban neighborhoods tend to outperform the national average. That description fits 92104.

None of this means prices will go up forever or that now is the “right” time for everyone. It means the dramatic crash some people are bracing for isn’t what the data shows.

What the Experts Are Saying (and Not Saying)

Most housing economists are calling 2026 a “reset year.” Not a boom. Not a bust. A recalibration.

The chief economist at Bright MLS described 2026 as “a year of cautious progress rather than a full housing rebound.” The chief economist at Redfin expects mortgage rates to stay around 6.3% and home prices to rise about 1% nationally.

Nearly 70% of agents in the HomeLight survey said they feel optimistic about the year ahead. At the same time, 47% of those same agents predict economic growth will remain slow. Those two things can be true at the same time. A slow economy does not automatically mean a bad housing market, especially in supply-constrained areas.

None of these experts is predicting a 2008-style crash. Homeowner equity is at record levels. Lending standards are sound. And inventory, while growing slightly, is still well below levels needed for prices to fall significantly in neighborhoods like North Park.

How to Think About Your Situation Instead of the Market’s Situation

Here is what most economic anxiety articles miss. The right decision for you has almost nothing to do with what the Federal Reserve does next.

It has everything to do with what is going on in your life. Your finances. Your goals. Your timeline.

Here are some questions to think about honestly:

Does your home still fit your life?

If you are rattling around in a house that is too big, or cramming a growing family into a space that is too small, the market is one factor among many. Your quality of life matters too. That doesn’t mean you should rush to list your home for sale right away. It simply means the answer to “should I move?” starts with your life, not a chart.

What does staying actually cost?

Staying is not free. Property taxes, insurance premiums, maintenance, and utilities are real monthly costs. If your insurance went up 15% to 20% this year (and many California homeowners saw increases in that range), that changes the financial picture. It does not mean you should sell. But it means “staying put” deserves the same honest financial look as moving would.

What does your equity look like?

If you bought your North Park home more than a few years ago, you likely have substantial equity. Knowing that number is valuable whether you decide to sell, refinance, tap a HELOC, or simply hold and do nothing. A home valuation is just information. Getting one does not commit you to anything. It just gives you a clearer picture of where you stand.

Are you making a decision or avoiding one?

This is the hardest question. Sometimes “waiting for the market to settle” is a reasonable strategy. Other times it’s a way of avoiding a decision that feels scary. Both are human. Recognizing which one you are doing lets you move forward with intention rather than drift.

What Fear-Based Decisions Look Like on Both Sides

Economic anxiety does not push everyone in the same direction. It pushes people to two extremes, and both can be costly.

Panic selling. Listing too quickly, underpricing because you think the sky is falling, and accepting the first offer that comes in on day 1, without a strategy or negotiating. This is how homeowners leave real money on the table.

If you are going to sell, it should be because your life circumstances support it, not because the media has scared the crap out of you.

Paralysis. Staying in a home that no longer works for you because you are afraid of making a mistake. Meanwhile, costs keep climbing, and your goals stay on hold. If you have been thinking about moving for two or three years but keep putting it off because the timing “does not feel right,” it is worth asking whether it ever will.

The better path is to try to stay neutral. Take this time to do your homework and get accurate information. Understand what your financial position is. Talk to people who know your neighborhood. Then make a conscious decision to either stay or wait, based on your actual circumstances. Not on what somebody said on a podcast last week.

A Few Things Worth Knowing Regardless of What You Decide

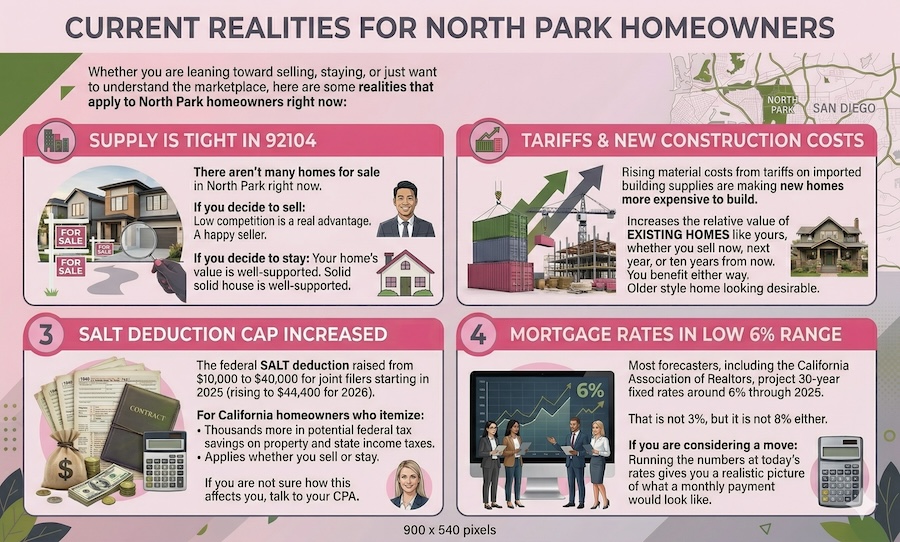

Whether you are leaning toward selling, staying, or just want to understand the marketplace, here are some realities that apply to North Park homeowners right now:

Supply is still tight in 92104. There aren’t many homes for sale in North Park right now. If you did decide to sell at this point, the low competition is a real advantage. If you decide to stay, it means your home’s value is well-supported.

Tariffs are raising new construction costs. Rising material costs from tariffs on imported building supplies are making new homes more expensive to build. That increases the relative value of existing homes like yours, whether you sell now, next year, or ten years from now. You benefit from this either way.

See what 2026 tariffs mean for North Park sellers and buyers.

The SALT deduction cap increased to $40,000. The “One Big Beautiful Bill” raised the federal SALT deduction from $10,000 to $40,000 for joint filers starting in 2025, with the cap rising to $40,400 for 2026. For California homeowners who itemize, this means thousands more in potential federal tax savings on property and state income taxes. This applies whether you sell or stay. If you are not sure how this affects you, talk to your CPA.

Mortgage rates are expected to stay in the low 6% range. Most forecasters, including the California Association of Realtors, project 30-year fixed rates around 6% through 2026. That is not 3%, but it is not 8% either. If you are considering a move at any point, running the numbers at today’s rates gives you a realistic picture of what a monthly payment would look like on the other side.

The One Mistake to Avoid No Matter What

The biggest mistake homeowners make during uncertain times is making rash decisions without doing their research.

Homeowners who sell without understanding their equity, their tax situation, and their local market often leave money on the table or rush into a bad deal. Homeowners who stay without understanding their carrying costs, their insurance exposure, or their options often end up feeling trapped when they did not need to be.

Information is free. A conversation with a local real estate agent. Feel free to contact the McT Real Estate Group if you have questions about the current market and your potential equity.

Also, a call to your CPA would be a good idea. A look at what comparable homes in your neighborhood have sold for recently. None of that obligates you to do anything. All of it puts you in a stronger position to make your own decisions.

You Do Not Have to Decide Right Now

There is no deadline. The market is not going to disappear overnight, and neither is your equity.

If you are not ready to make a move, that is completely fine. But consider getting the information now so that when you are ready, whether that is next month or next year, you are working from facts instead of starting from scratch.

We have spoken to some of our clients for years before actually selling their homes in North Park and other metro neighborhoods. As a matter of fact, we just sold a Spanish-style casita to a client on Oregon Street, with whom we’ve been in communication for at least 7 years.

Every now and then, we would chat about the market and her future plans. And guess what? Her future plans arrived. We got together and put a strategic plan into place. Put her home on the market, received multiple offers, and she received $50,000 over list price. She was able to move on to the next chapter of her life, which is in another area of Southern California.

If you want to know what your home is worth, get your Free Home Valuation.

If you want to have an honest conversation about what is happening in 92104, we are here. No pressure. No pitch. Just real answers from someone who has been helping homeowners in North Park for over 20 years.

Reach out to McT Real Estate Group whenever you are ready. Or don’t. Either way, we hope this helped you think a little more clearly about where you stand.

Frequently Asked Questions

Is 2026 a bad time to be a homeowner in North Park?

No. North Park remains one of the most supply-constrained neighborhoods in San Diego, with inventory well below balanced-market levels. Home values in San Diego County are up 2.1% year over year, and the neighborhood continues to attract strong buyer interest. Being a homeowner in 92104 is still a solid position, regardless of the national economic noise.

Should I sell my North Park home because I am worried about a recession?

Fear of a recession alone is not a strong reason to sell. Most forecasters, including J.P. Morgan and the National Association of Realtors, say a full recession is unlikely in 2026. If your reasons for considering a sale are personal, like downsizing, relocating, or needing more space, those reasons stand on their own merit. If your only reason is fear of a downturn, getting a clear picture of your home’s current value can help you think through it more calmly.

How do I know if I should sell or stay in my home?

Start with your life situation, not the market. Does your home still fit how you live? Can you comfortably afford the carrying costs? Are your goals being served by staying, or are they delayed by it? The market is one input. Your finances, your family, and your long-term plans are bigger ones. A conversation with a local real estate professional and your financial advisor can help you weigh all of those factors together.

Will tariffs cause home prices to drop in North Park?

Tariffs on imported building materials raise the cost of new construction, but they do not directly lower the value of existing homes. In fact, higher construction costs can make existing homes relatively more attractive to buyers. North Park’s housing stock is almost entirely existing homes, so this dynamic works in your favor whether you sell or hold. The broader San Diego market is adjusting to tariff-related cost pressures, but supply constraints in 92104 continue to support values.

What is the smartest thing a North Park homeowner can do right now?

Get informed. Know what your home is worth. Understand how much equity your home has. Review your insurance and carrying costs. Talk to your CPA about the new SALT deduction changes. You do not have to act on any of this information right away. But having it means you are ready to make a confident decision whenever your situation calls for one, instead of scrambling when things feel urgent.

Z. McT-Contreras | McT Real Estate Group | DRE #01715784