North Park home values are holding steady this spring. Detached inventory remains tight. But buyers are more selective than they were two years ago. With 30-year fixed rates hovering between 6.1 and 6.4 percent as of mid-April 2026, affordability is on every buyer’s mind. One strategy that more North Park sellers should understand is the mortgage rate buydown.

If a buyer asks you to fund a rate buydown, should you say yes? And could offering one proactively help you sell faster without cutting your price? Here is what sellers in 92104 need to know.

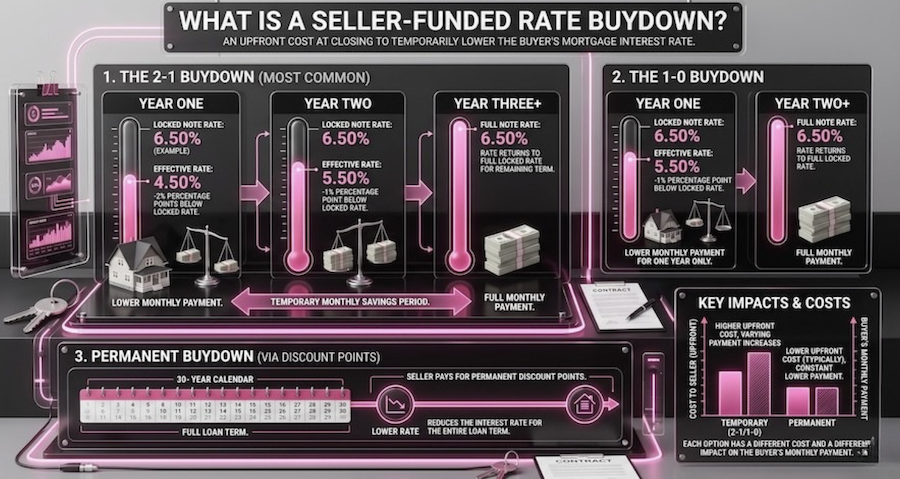

What Is a Seller-Funded Rate Buydown?

A rate buydown is when the seller pays an upfront cost at closing to temporarily lower the buyer’s mortgage interest rate. The most common version is the 2-1 buydown. In year one, the buyer’s rate drops by 2 percentage points below their locked rate. In year two, it drops by 1 point. By year three, the rate returns to the full note rate.

There is also a 1-0 buydown, which lowers the rate by 1 point in the first year only. Some sellers offer a permanent buydown by paying discount points, which reduces the rate for the entire loan term. Each option has a different cost and a different impact on the buyer’s monthly payment.

How the Math Works on a North Park Home

Take a $1 million North Park Craftsman with 20 percent down. The buyer is financing $800,000. At a 6.3 percent rate, their monthly principal and interest payment is roughly $4,954.

With a 2-1 buydown funded by the seller, the buyer pays as if the rate were 4.3 percent in year one. That brings month one’s payment down to about $3,961. In year two, the rate steps up to 5.3 percent, and the payment rises to roughly $4,440. By year three, the buyer is at the full 6.3 percent rate.

The cost to the seller for this 2-1 buydown is typically around $15,000 to $18,000, depending on the lender. That money is held in escrow and used to subsidize the buyer’s payments during the buydown period.

Why This Beats a Price Reduction

This is the part most sellers miss. Dropping your price by $15,000 on a $1 million home saves the buyer about $80 per month on their mortgage. That same $15,000 used as a 2-1 buydown saves them roughly $1,000 per month in year one. The buyer feels a much bigger impact from the buydown.

There is another advantage. Your sale price stays at $1 million. That matters for your net proceeds, and it matters for comparable sales in your neighborhood. When your home closes at a higher recorded price, it supports property values for your neighbors and for future sellers on your block. If you are already weighing whether to price slightly below comps to attract more buyers, a buydown gives you a third option worth considering.

When a Buydown Makes Sense for Sellers

A seller-funded buydown is not always the right move. It works best in specific situations.

- Your home has been listed for four or more weeks with limited offers, and you want to attract attention without lowering your price.

- You are selling an attached unit or condo where buyer demand is softer, and rate sensitivity is higher.

- A buyer submits a strong offer but asks for a concession. A buydown may cost you less than a price cut and give the buyer more value.

- You are competing with newer listings that have fresh marketing momentum.

If your home is already generating multiple offers, there is no need to offer a buydown. Let the market work for you. Our guide on how to negotiate multiple offers in North Park covers that scenario in detail.

What North Park Sellers Should Watch Out For

Not every lender handles buydowns the same way. Some lenders have restrictions on temporary buydowns, and the buyer’s qualifying rate may still be based on the full note rate. That means a buydown does not always help a buyer qualify for a larger loan. It helps them with cash flow in the early years.

Also, a buydown is a concession. It counts toward the total seller concessions allowed by the loan program. For conventional loans with 20 percent down, the cap is typically 9 percent of the sale price. For FHA loans, it is 6 percent. Your agent and the buyer’s lender need to coordinate to ensure the buydown does not push the concessions over the limit. For a full breakdown of what sellers pay at closing, see our North Park seller closing costs guide.

In my 20+ years of listing homes in North Park and 530+ closed transactions, I have seen sellers leave money on the table by seeking a price cut when a buydown would have been more effective. Talk with your listing agent about whether a buydown, closing cost credit, or price adjustment gives you the best net outcome for your specific situation. The right answer depends on your home’s price point, condition, and how the market is responding to your listing.

The Bottom Line

In a spring 2026 market where rates are shaping buyer behavior, a seller-funded rate buydown is one of the most underused tools available. It lets you keep your sale price intact while giving buyers the monthly payment relief they are looking for.

For North Park homeowners thinking about listing this spring, understanding concession options like buydowns puts you in a stronger negotiating position. Start with a conversation and a clear picture of your home’s current value. If the price is right and the marketed well, you won’t even need to think about using this strategy.

Ready to plan your sale? Call and schedule a phone call today at mctrealestategroup.com. You can also read our complete guide to selling your home in North Park to see how buydowns fit into a full listing strategy.

Frequently Asked Questions

What does a 2-1 buydown cost the seller?

On a typical North Park home with an $800,000 loan, a 2-1 buydown costs the seller roughly $15,000 to $18,000. The exact amount depends on the base interest rate and the lender’s calculation method. This money is placed in an escrow account at closing.

Is a buydown better than lowering my asking price?

In most cases, a buydown gives the buyer a bigger monthly savings per dollar spent than a straight price cut. A $15,000 price reduction saves the buyer about $80 per month. That same $15,000 as a 2-1 buydown can save around $1,000 per month in year one. Your sale price also stays higher, which helps your net and neighborhood comps.

Can a seller offer a buydown proactively in the listing?

Yes. Some listing agents advertise a seller-funded buydown in the MLS remarks or marketing materials to attract rate-sensitive buyers. This can generate more showings and stronger initial interest, especially for homes priced above $900,000 where rate changes have a larger effect on monthly payments.

Does a buydown help the buyer qualify for a bigger loan?

Not always. Most lenders qualify the buyer at the full note rate, not the temporarily reduced rate. The buydown helps with monthly cash flow in the first one to two years, but it does not typically increase the buyer’s purchasing power. Check with the buyer’s lender for their specific guidelines.

How does a buydown affect my net proceeds as a seller?

A buydown is a cost at closing, just like a closing cost credit or repair concession. It reduces your net proceeds by the buydown amount. However, because it often allows you to hold your sale price higher than you would with a price reduction, the net result can be better than cutting the price by the same amount. Our step-by-step guide to selling in San Diego walks through how concessions factor into your final net.

About the Author

Z. McT-Contreras is the co-founder of the McT Real Estate Group and a North Park listing specialist with over 20+ years of residential real estate experience in San Diego. She has personally guided more than 530 homeowners through successful home sales across North Park (92104), South Park, University Heights, Normal Heights, Golden Hill, and Mission Hills.

Z works exclusively with sellers and a small group of buyers, focusing on Craftsman bungalows, Spanish-style homes, and Mills Act-designated properties built between 1900 and 1940. Her seller-first approach, hyper-local 92104 pricing strategy, and full-service marketing have helped North Park homeowners net top dollar in every market cycle since 2004.

If you are thinking about selling your North Park home, you can request a free home valuation or schedule a no-pressure consultation with Z directly.

Z. McT-Contreras | McT Real Estate Group

DRE#01715784