Can an insurance problem kill your North Park home sale? Yes. Buyers who cannot secure homeowners’ insurance cannot close their loan. That means delayed escrows, canceled deals, and surprise concessions for sellers in 92104.

North Park, San Diego, homeowners are watching something new unfold in real estate transactions. Deals that would have closed easily two years ago are now hitting insurance roadblocks. Buyers are dropping out. Escrows are extending. Sellers are getting calls from their agents mid-transaction asking for help.

If you are thinking about selling, you need to understand this before you list.

For a broader overview of the selling process, our North Park seller’s guide walks through what to expect.

What Is Happening With Home Insurance in California Right Now

California’s home insurance market is in the middle of its biggest shakeup in decades. Several major carriers have paused new policies or non-renewed existing ones. Premiums are climbing. And the FAIR Plan, which is supposed to be a backstop for high-risk properties, is overloaded.

According to KPBS reporting, some buyers are unable to secure insurance within the 30 to 45-day escrow window due to a lack of available options and slow FAIR Plan response times.

The California Department of Insurance is pushing reforms through the Sustainable Insurance Strategy and the Make It FAIR Act. Those changes are aimed at bringing carriers back and stabilizing rates. But the market has not stabilized yet. Until it does, every transaction carries some insurance risk.

How This Affects a North Park Home Sale

North Park is not a high-risk wildfire zone like canyon-adjacent neighborhoods in East County or the hillsides of LA. That is good news. But insurance issues still appear in North Park transactions, and sellers should know where.

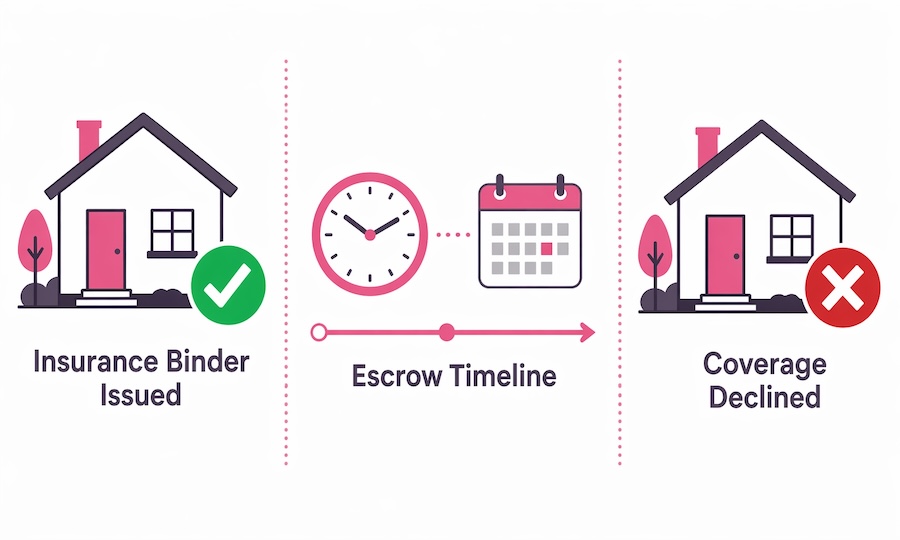

Escrow Delays

A standard escrow runs 30 to 45 days. Buyers typically secure insurance in the last two weeks. If a carrier takes 3 weeks to underwrite, or if the buyer has to switch to the FAIR Plan mid-transaction, escrow gets pushed out.

For sellers, that means your closing date moves. If you are coordinating a move-up purchase or a 1031 exchange, a delay can cascade into other problems.

Buyer Qualification Issues

Here is the one that catches sellers off guard. If insurance premiums come back higher than expected, the buyer’s debt-to-income ratio changes. Lenders include property insurance in the housing cost calculation. A $2,000 annual premium becoming $4,500 can push a buyer out of loan qualification.

When that happens, the buyer cannot close. The deal dies. The seller returns to the market, and the listing now shows a canceled contract in its history.

Repair Requests Tied to Insurability

Many older North Park bungalows have features that insurance carriers flag. Roofs over 20 years old. Unpermitted work. Aging electrical panels. Outdated plumbing. Original wood siding.

Carriers are increasingly requiring repairs before issuing a binder. That pressure flows back to the seller. We are seeing buyers ask for credits or repairs during escrow that they would not have asked for a few years ago.

What Sellers in 92104 Should Do Before Listing

You cannot control the insurance market. But you can control how prepared your home is to pass an underwriter’s review. A few steps before listing can prevent a deal from falling apart in escrow.

Check Your Roof Age

If your roof is over 20 years old, most carriers will flag it. Some will decline coverage outright. Before listing, know your roof’s age and condition. If it is near the end of life, pricing this in upfront is better than handling it in escrow.

Address Obvious Hazards

Steps without railings. Broken concrete walkways. Dead trees near the house. Missing smoke or carbon monoxide detectors. These are quick fixes that carriers and inspectors will notice.

Pull Your Own CLUE Report

A Comprehensive Loss Underwriting Exchange report shows your home’s claims history. If there are old claims you forgot about, they can affect the next buyer’s ability to get insurance. Knowing in advance gives you time to prepare.

Get a Pre-Listing Inspection

This is the single best protection against insurance-related escrow surprises. A good inspection surfaces everything a carrier might flag. You can fix what needs fixing, disclose the rest, and price the home accordingly.

For more on pricing, take a look at our expert predictions on residential home prices for the current market context.

What Buyers Are Doing Differently Now

Smart buyers in San Diego are starting their insurance search the day their offer is accepted. Some are even getting preliminary quotes before making offers. This is a change from five years ago, when insurance was an afterthought handled in the last week of escrow.

If a buyer brings up insurance early in your transaction, that is actually a good sign. It means they are serious and prepared.

As a seller, you should expect your listing agent to coordinate with the buyer’s side early on insurance. Ours does. That early coordination prevents last-minute panic.

Frequently Asked Questions About Insurance and Home Sales in North Park

Can a buyer back out of a home purchase due to insurance issues?

Yes, if the buyer has an insurance contingency in the contract. Most California residential purchase agreements allow the buyer to cancel during the contingency period if they cannot secure acceptable insurance at a reasonable cost. Once contingencies are removed, canceling gets more complicated.

Does North Park have high insurance risk?

North Park is not in a Very High Fire Hazard Severity Zone like some canyon or hillside neighborhoods. Most homes here can still get standard coverage. However, older bungalows with aging roofs, electrical systems, or unpermitted work can face higher premiums or coverage challenges.

What if a buyer can only get FAIR Plan coverage?

The FAIR Plan is fire-only coverage. It does not cover theft, liability, or water damage. Lenders often require a DIC (Difference in Conditions) policy to fill the gaps. That combination is more expensive and harder to coordinate, which can slow escrow.

Should I replace my roof before selling my North Park home?

If your roof is over 20 years old or showing wear, replacing it before listing often pays off. You avoid escrow surprises, expand your buyer pool, and can price the home with confidence. If replacement is not in your budget, get a roof certification to document the current condition.

How early should I get my home ready for insurance scrutiny?

Start 60 to 90 days before listing. That gives you time for a pre-listing inspection, repairs, roof evaluation, and any improvements to obvious hazards. Waiting until you are in escrow to address these issues is where deals go sideways.

The Bottom Line for North Park Homeowners

The insurance market is not what it used to be. That does not mean your North Park home will not sell. It means you need a listing strategy that accounts for insurance as part of the transaction, not just a final step.

Most North Park homes still find insurance. Most deals still close. But the sellers and their listing agents who prepare in advance are the ones whose transactions are not derailed by a last-minute insurance surprise.

Call and schedule a phone call today. McT Real Estate Group has been helping North Park homeowners close deals cleanly for over 20 years.

Z. McT-Contreras | McT Real Estate Group | DRE #01715784